Cushman & Wakefield, a global real estate services company, has released its Asia Pacific Data Centre H1 2024 Update.

The report shows the Asia Pacific data centre market1 recorded 1.3GW of new supply in the first six months of the year, to reach a current operational capacity of 11.6GW.

Malaysia, predominantly Johor, saw the greatest increase in operational capacity, up 80% from H2 2023. The Head of Cushman & Wakefield’s Data Centre Advisory Team in Asia Pacific, Vivek Dahiya, said:\

“Malaysia’s recent growth is the result of a culmination of factors including spillover from Singapore, developer speed to market and the country’s ‘ready for service’ infrastructure. Cost is also a major factor. Malaysia’s central bank rate is competitive and this, combined with a relatively affordable cost of entry and government incentives for the sector, make it an appealing location for customers from hyperscalers through new entrants to the sector.”

The influence of technological advancements such as the implementation of cloud computing, deployment of 5G networks, government digitization initiatives and increasing mobile and internet penetration, especially in fast growing populations, have significantly accelerated the demand for data centres globally.

In Asia Pacific, the largest six markets account for ~85% of operational capacity. Sydney is the fastest growing market in Asia Pacific by megawatt growth, adding 177MW in operational capacity in H1.

The development pipeline2 includes 4.2GW of under construction activity and 12.0GW in the planning stage. This represents an increase of 2.8GW in development activity since end-H2 2023.

Asia Pacific market data

Figure 1: Largest markets by operational

capacity

|

Rank

|

Geography

|

Capacity (MW)

|

Capacity (GW)

|

|

1

|

Chinese mainland

|

4,199

|

4.20

|

|

2

|

Japan

|

1,423

|

1.40

|

|

3

|

India

|

1,406

|

1.40

|

|

4

|

Australia

|

1,230

|

1.20

|

|

5

|

Singapore

|

985

|

0.99

|

|

6

|

South Korea

|

649

|

0.65

|

|

7

|

Hong Kong, China

|

584

|

0.58

|

|

8

|

Malaysia

|

349

|

0.35

|

|

9

|

Indonesia

|

296

|

0.30

|

|

10

|

Taiwan, China

|

246

|

0.25

|

Figure 2: Largest markets by total market size

(including operational, under construction and planned)

|

Rank

|

Geography

|

Capacity (MW)

|

Capacity (GW)

|

|

1

|

Chinese mainland

|

6,515

|

6.52

|

|

2

|

India

|

4,336

|

4.34

|

|

3

|

Japan

|

4,059

|

4.06

|

|

4

|

Australia

|

3,278

|

3.28

|

|

5

|

Malaysia

|

3,108

|

3.11

|

|

6

|

South Korea

|

1,727

|

1.73

|

|

7

|

Singapore

|

1,334

|

1.33

|

|

8

|

Hong Kong, China

|

1,127

|

1.13

|

|

9

|

Indonesia

|

1,046

|

1.05

|

|

10

|

Thailand

|

467

|

0.47

|

Figure 3: Largest cities by total market size

(including operational, under construction and planned)

|

Rank

|

Geography

|

Capacity (MW)

|

Capacity (GW)

|

|

1

|

Beijing

|

2,919

|

2.92

|

|

2

|

Tokyo

|

2,725

|

2.73

|

|

3

|

Shanghai

|

2,050

|

2.05

|

|

4

|

Sydney

|

1,993

|

1.99

|

|

5

|

Mumbai

|

1,831

|

1,83

|

|

6

|

Singapore

|

1,334

|

1.33

|

|

7

|

Seoul

|

1,231

|

1.23

|

|

8

|

Hong Kong, China

|

1,127

|

1.13

|

|

9

|

Johor

|

1,898

|

1.90

|

|

10

|

Kuala Lumpur

|

1,094

|

1.09

|

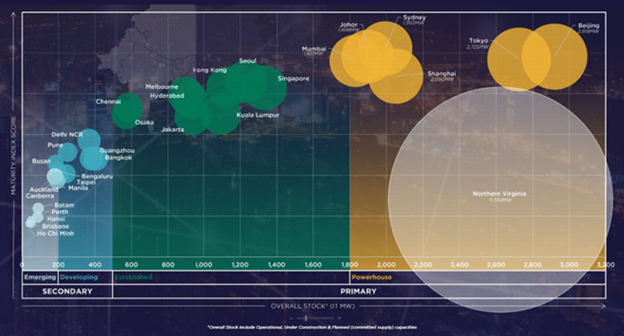

Market maturity index

Figure 4: Market Maturity Index

Cushman & Wakefield’s Asia Pacific

Maturity Index tracks 30 data centre markets across Asia Pacific to assess both

their current maturity and their future potential3.

Powerhouse markets are Sydney, Johor, Beijing, Tokyo,

Mumbai and Shanghai.

-

Sydney is considered the most mature market in the region,

based on a combination of variables including size, vacancy rate,

operator presence and individual asset level build capacities. While

Beijing and Tokyo have tighter vacancy levels, Sydney scores higher for

its larger build capacity (scale of individual data centres), which is an

indicator of future strength considering impending AI deployments.

- Johor ranks as the second most mature market, considering

very low vacancy at 2% and with the highest build capacity amongst all

markets.

Established markets are Seoul, Hong Kong China, Singapore,

Melbourne, Hyderabad, Chennai, Kuala Lumpur, Osaka and Jakarta. These

prominent markets have either exceeded 1.0GW size, or are approaching

1.0GW. Many of these markets benefit from strategic geographic locations

and connectivity.

-

These established markets are witnessing continued

interest by the American hyperscale cloud entities, with all markets

having presence or committed pipeline of at least one or two of the

entities; Singapore has three.

Developing markets,

Delhi, Pune, Guangzhou, Bangkok, Bengaluru, Taipei, Manila, typically have

smaller live capacities. These markets typically have higher vacancies because

the absorption rates are slower than the addition of new supply.

Emerging markets cumulatively account for about 3% of the

total operational capacity in APAC. The under-construction pipeline for

these markets remains in the single digits as operators wait for further

evidence of demand before converting planned capacity into operational.

1 “Asia Pacific” refers to Australia, Chinese mainland, Hong Kong China, India, Indonesia, Japan, Malaysia, New Zealand, Philippines, Singapore, South Korea, Taiwan,China, Thailand and Vietnam.

2 Operational capacity refers to data centres in operation. Development pipeline figures include projects that are both under construction and planned.

3 The methodology has been refined in H1 2024 to accommodate the impact of AI on the sector, and feedback from clients.

Source: Cushman& Wakefield